We appreciate investors are faced with some difficult decisions, particularly with cash and fixed interest investments expected to offer low returns for some time. However, we encourage them to view…

How many years of spending can your Investment Wealth support? This is our third article in a series of six that examines the rationale for each chart included on a…

Lifetime Annuities: good product, immature market If you’re looking for a way to outsource your investment, longevity and inflation risks, you’re in luck. There is a financial product (a lifetime…

Retirement spending estimation is more than a financial exercise In a previous article, “What is an appropriate Retirement Expenditure Multiple?”, we suggested that a figure of 25 times your desired…

Some suggest a retirement expenditure multiple as low as 12 … When clients ask us how much wealth they need to accumulate to ensure a high chance of meeting their…

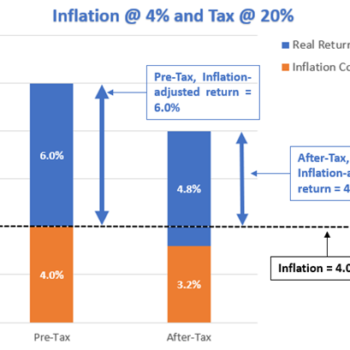

A picture paints a thousand words… Our recent article, “What is “The Value of Financial Planning”?”, introduced a number of key metrics that we monitor to assess clients’ progress toward…